A comprehensive investigation into the wave of cyberattacks devastating mortgage lenders from 2023-2025

The American dream of homeownership has become a nightmare for tens of millions of consumers. Between October 2023 and October 2025, a relentless wave of cyberattacks has compromised the most sensitive financial data of over 47 million Americans—targeting the very institutions entrusted to protect their path to homeownership.

From industry giants managing nearly trillion-dollar portfolios to regional lenders, the mortgage sector has proven to be a goldmine for cybercriminals. These aren’t isolated incidents—they represent a systemic failure in an industry that handles some of the most sensitive personal and financial data imaginable: Social Security numbers, bank account details, dates of birth, and complete financial histories.

What makes these breaches particularly devastating is their scope. Unlike typical data breaches where current customers are affected, mortgage lenders retain records spanning decades. When Mr. Cooper Group was breached in 2023, it exposed data from customers dating back to 2001—people who paid off their mortgages nearly two decades ago suddenly found themselves at risk of identity theft.

This investigation examines nine major mortgage breaches, revealing troubling patterns of inadequate security, delayed notifications, third-party vulnerabilities, and an industry ill-prepared to defend against sophisticated ransomware gangs.

The Numbers Tell a Devastating Story

Before diving into individual incidents, let’s understand the scale of destruction:

- Total Victims: 47+ million individuals

- Largest Single Breach: LoanDepot - 16.9 million victims

- Settlement Costs: $86.6+ million (and counting)

- Response Costs: $50+ million in forensic investigations and recovery

- Primary Threat Actors: Black Basta ransomware gang, ALPHV/BlackCat gang

- Average Notification Delay: 2-3 months from detection

- Data Types Compromised: Names, Social Security numbers, dates of birth, bank account numbers, driver’s licenses, financial account details, email addresses, phone numbers

Mr. Cooper Group: When the Biggest Falls Hardest

Breach Timeline: October 30 - November 1, 2023 Detection: October 31, 2023 Victims: 14.7 million individuals Cost to Company: $25+ million

The Mr. Cooper Group breach stands as a cautionary tale of how quickly trust can evaporate. As the largest non-bank mortgage servicer in America with a $937 billion servicing portfolio and 4.3 million active customers, Mr. Cooper represented the pinnacle of the industry—until unauthorized actors spent three days inside their systems.

What Happened

On October 31, 2023, Mr. Cooper detected “suspicious activity” on its network. The company immediately shut down multiple systems, including the online payment portals that millions of customers relied on to make their mortgage payments. What initially appeared to be a limited “isolated incident” quickly spiraled into one of the largest financial data breaches in U.S. history.

The forensic investigation revealed a devastating truth: the attackers had accessed “substantially all” current and former customer records. This wasn’t just a breach of active accounts—it was a complete compromise of the company’s historical data repository.

The Data Exposed

Every piece of information needed for comprehensive identity theft was stolen:

- Full names and home addresses

- Social Security numbers

- Dates of birth

- Phone numbers

- Bank account numbers

The Hidden Victims

Perhaps most shocking was the breadth of victims. Mr. Cooper’s data retention practices meant that anyone who had ever:

- Been a current or former Mr. Cooper customer

- Had a mortgage serviced by sister brands (RightPath Servicing, Rushmore Servicing, Greenlight Financial Services, Champion Mortgage)

- Had loans acquired or serviced by predecessor companies Nationstar Mortgage LLC (dating to 2006) or Centex Home Equity (dating to 2001)

One Reddit user captured the absurdity: “This was so odd to me as the last time I applied for a mortgage was 2005 and I haven’t had a mortgage since 2010 when I paid off my house. Why the hell are they still storing my social security number after almost 14-19 years?”

The Aftermath

Mr. Cooper’s response costs ballooned from an initial estimate of $5-10 million to $25 million, which included:

- Forensic investigation expenses

- System restoration and security enhancements

- Two years of free credit monitoring through TransUnion for all 14.7 million victims

- Legal defense costs for ongoing class action litigation in Texas

The company claims to be monitoring the dark web with “no evidence” the data has been further shared or misused—a claim that provides cold comfort to millions whose most sensitive information is now in criminal hands.

LoanDepot: The Ransomware Gang That Broke the Bank

Breach Timeline: January 3-5, 2024 Detection: January 4, 2024 Victims: 16.9 million individuals Threat Actor: ALPHV/BlackCat ransomware gang Total Settlement: $86.6 million

LoanDepot’s breach represents the most expensive mortgage data breach settlement in history and demonstrates why ransomware has become the weapon of choice for cybercriminals targeting financial institutions.

The Attack

On January 4, 2024, LoanDepot—the nation’s fifth-largest retail mortgage lender—identified a “potential security incident” and immediately took multiple systems offline. The forensic investigation revealed that between January 3rd and 5th, an unauthorized third party had not only accessed their systems but had deployed ransomware that encrypted files across compromised systems.

On February 16, 2024, the ALPHV/BlackCat ransomware gang publicly claimed responsibility for the attack, confirming what many security experts had suspected: this was a sophisticated ransomware operation designed for maximum damage and extortion potential.

The Scope of Devastation

The 16.9 million victims included not just current customers, but a disturbing number of people who had no known connection to LoanDepot. Multiple recipients of breach notifications took to Reddit expressing shock:

“I’ve never had a mortgage, never applied for one, and never even heard of LD [Loan Depot]. The only loans I have are school loans.”

This revelation suggests that LoanDepot’s data collection practices extended far beyond its direct customer base—possibly through third-party data aggregation, partner networks, or acquisitions of other lenders’ customer databases.

The Compromised Data

The attackers obtained a complete identity theft toolkit:

- Names and home addresses

- Email addresses and phone numbers

- Dates of birth

- Social Security numbers

- Financial account numbers

The Legal Reckoning

In what became a landmark settlement, LoanDepot faced a California class action lawsuit alleging the company’s poor cybersecurity practices were directly responsible for the breach. The plaintiffs argued that LoanDepot:

- Failed to implement adequate cybersecurity measures

- Did not properly train employees

- Retained unnecessary customer data for extended periods

- Failed to adequately monitor for threats

While LoanDepot admitted no wrongdoing, the company agreed to an $86.6 million settlement package:

$25 Million Cash Settlement Fund:

- $5.30 to $70.71 per affected individual (depending on participation rate)

- California residents eligible for additional $14.90 to $149.04 under CCPA provisions

- Up to $5,000 reimbursement for documented out-of-pocket expenses

- Two years of financial monitoring and identity theft insurance services

$9.34 Million in Business Improvements:

- Enhanced data management systems

- Increased cloud security infrastructure

- Improved threat detection capabilities

- Better identity protection measures

Settlement Timeline:

- Exclusion/Objection Deadline: April 27, 2025

- Claims Deadline: May 27, 2025

- Final Approval Hearing: August 18, 2025

The Response Costs

Beyond the settlement, LoanDepot acknowledged $27 million in direct response costs, not including lost revenue during system downtime. The company’s stock took a significant hit, and its reputation within the industry suffered lasting damage.

Black Basta’s Reign of Terror: McLean Mortgage & MIG

Two mortgage lenders fell victim to the same sophisticated ransomware gang—Black Basta—demonstrating how organized cybercrime groups systematically target vulnerable industries.

McLean Mortgage Corporation: The Company That Didn’t Survive

Breach Timeline: October 17, 2024 Detection: October 17, 2024 Victims: 30,453 individuals Threat Actor: Black Basta ransomware gang Company Status: Appears to have ceased operations

McLean Mortgage Corporation’s story is particularly tragic—a Virginia-based lender founded in 2008 that couldn’t survive the aftermath of a catastrophic breach.

The Attack:

On October 17, 2024, McLean Mortgage identified suspicious activity on its network. The subsequent investigation confirmed every CISO’s nightmare: Black Basta had infiltrated their systems and exfiltrated approximately 1 terabyte of data.

The stolen data included:

- Customer personal information (names, SSNs, driver’s licenses, financial accounts)

- Accounting records and financial data

- Complete loan details and documentation

- Payroll information

- Tax documents

- Human resources files

- Confidential business data

- Personal documents of both customers and employees

The Dark Web Threat:

Black Basta announced on the dark web that they had compromised McLean’s systems and threatened to publish the stolen data within 7-8 days unless ransom demands were met. The gang specifically claimed to have stolen highly sensitive data including customer SSNs and financial records.

Investigation Timeline:

- October 17, 2024: Breach detected

- May 12, 2025: Investigation completed (7 months)

- June 11, 2025: Notifications began

The Legal Fallout:

Four separate federal class action complaints were filed against McLean Mortgage, seeking over $5 million in damages. The lawsuits alleged:

- Negligence in protecting customer data

- Failure to implement reasonable cybersecurity measures

- Violation of state and federal data protection laws

- Breach of fiduciary duty

The Company’s Demise:

By mid-2025, McLean Mortgage appears to have gone out of business. The company:

- Had no active origination licenses in 2025

- Voluntarily surrendered Virginia state licenses in October 2024 (weeks after the breach)

- Ceased operations while class action litigation remained pending

This raises troubling questions about accountability: What happens to ongoing lawsuits when the defendant company no longer exists? Who compensates the 30,453 victims? Where does their stolen data end up when there’s no company left to monitor the dark web?

Mortgage Investors Group (MIG): Black Basta Strikes Again

Breach Timeline: December 11, 2024 Detection: December 12, 2024 (early morning) Victims: Number undisclosed Threat Actor: Black Basta ransomware gang

Just two months after devastating McLean Mortgage, Black Basta targeted another mortgage lender—Tennessee-based Mortgage Investors Group.

The Attack:

MIG, a trusted mortgage lender serving the Southeast since 1989, detected the breach within hours of the initial intrusion—a faster response than many victims manage. On December 12, 2024, at approximately 2 AM, MIG’s security systems flagged unauthorized access. The company immediately shut down network access and secured systems, successfully terminating the unauthorized access.

The Investigation:

MIG engaged external cybersecurity forensics experts and completed their investigation by December 30, 2024—a relatively swift 18-day turnaround. The forensic analysis confirmed that on December 11, an unauthorized third party gained access to MIG’s systems, potentially exposing:

- Full names

- Financial information (specific types not yet disclosed)

The Company Response:

MIG’s response earned some praise for its transparency and speed:

- Immediate public disclosure via press release (January 20, 2025)

- Dedicated breach webpage with ongoing updates

- Dedicated support hotline: (877) 739-0798

- Two years of free credit monitoring through TransUnion

- Direct engagement with law enforcement and regulators

Statement from Leadership:

Anna Beltran, President and CEO of MIG, stated: “At Mortgage Investors Group, our commitment to our customers is for life. Protecting their personal information is central to our mission, and we are taking every possible step to address this incident thoroughly and responsibly.”

However, as of October 2025, MIG still has not disclosed the total number of affected individuals—a concerning omission nearly 10 months after the breach.

Black Basta’s Pattern:

The fact that Black Basta successfully attacked two mortgage companies within two months reveals:

- Systematic targeting of the mortgage industry

- Exploitation of common vulnerabilities across similar institutions

- Successful business model for the ransomware gang

- Industry-wide security deficiencies that multiple lenders share

Black Basta has been on federal law enforcement’s radar since at least 2022, with agencies warning that the group targeted 12 of 16 critical infrastructure sectors and attacked at least 500 organizations globally between April 2022 and May 2024.

The Third-Party Nightmare: New American Funding & Mobile Notary Zone

Breach Timeline: Suspicious activity discovered June 6, 2025 Actual Breach: Unknown timeframe Victims: Unknown (NAF unable to determine exact number) Vulnerability: Third-party vendor Mobile Notary Zone

New American Funding’s breach illustrates one of cybersecurity’s most insidious vulnerabilities: the supply chain attack. NAF’s own systems remained secure, yet thousands of customers found their most sensitive data compromised through a vendor they’d never heard of.

What Happened

On June 6, 2025, New American Funding discovered “suspicious activity associated with information provided to one of our vendors that provided notary services”—Mobile Notary Zone (MNZ). The discovery was likely triggered by either:

- Notification from law enforcement

- Reports from other affected companies

- Dark web monitoring alerts

- Direct notification from MNZ itself (though the vendor “provided little information”)

The Vendor Relationship

Mobile Notary Zone provided critical services for NAF’s loan closing process—handling notarization of loan documents, which inherently required access to complete customer information:

- Full names and addresses

- Social Security numbers

- Dates of birth

- Financial account information

- Complete loan documentation

- Government-issued IDs

When consumers signed their closing documents, they were interacting with MNZ’s systems, not NAF’s—but few customers had any idea their data was being shared with a third party.

The Compromised Data

An “unauthorized actor gained access to systems containing New American Funding consumer data and may have taken documents.” The stolen loan closing documents likely contained:

- Complete customer applications

- Proof of income and employment

- Bank statements

- Tax returns

- Credit reports

- Property information

- Signed legal agreements

NAF’s Impossible Position

New American Funding found itself in a uniquely frustrating situation:

- Their own systems were never breached

- They had no control over MNZ’s security practices

- They couldn’t determine which specific customers were affected

- MNZ provided minimal cooperation or information

Because NAF couldn’t identify individual impacted customers, they took the extraordinary step of notifying all customers whose information had ever been shared with MNZ—potentially over-notifying thousands of unaffected customers to ensure no actual victims were missed.

The Swift Response

To NAF’s credit, they:

- Immediately terminated their relationship with MNZ on June 6

- Alerted law enforcement and federal regulators

- Completed internal review within 20 days (by June 26)

- Filed disclosure with California AG on July 11

- Began customer notifications immediately

The Broader Implications

The Mobile Notary Zone breach sent shockwaves through the real estate and lending industries. The California League of Independent Notaries issued a public statement warning:

“This is a critical moment to reaffirm our collective commitment to ethical, transparent, and secure notarial practices. Notaries must advocate for stronger guardrails that protect client information and empower notaries to maintain professional independence.”

The incident highlighted several critical issues:

- Lack of vendor oversight: How many other mortgage lenders use MNZ?

- Inadequate due diligence: Were MNZ’s security practices ever audited?

- Regulatory gaps: Who oversees the cybersecurity of notary service providers?

- Disclosure failures: MNZ’s silence left multiple companies and thousands of consumers in the dark

Other Affected Organizations

NAF wasn’t the only victim. The breach appeared to impact multiple organizations that used MNZ’s services, including payroll providers and other mortgage lenders. The full scope of MNZ’s breach remains unknown—the vendor apparently collapsed under the weight of the incident without ever providing complete disclosure.

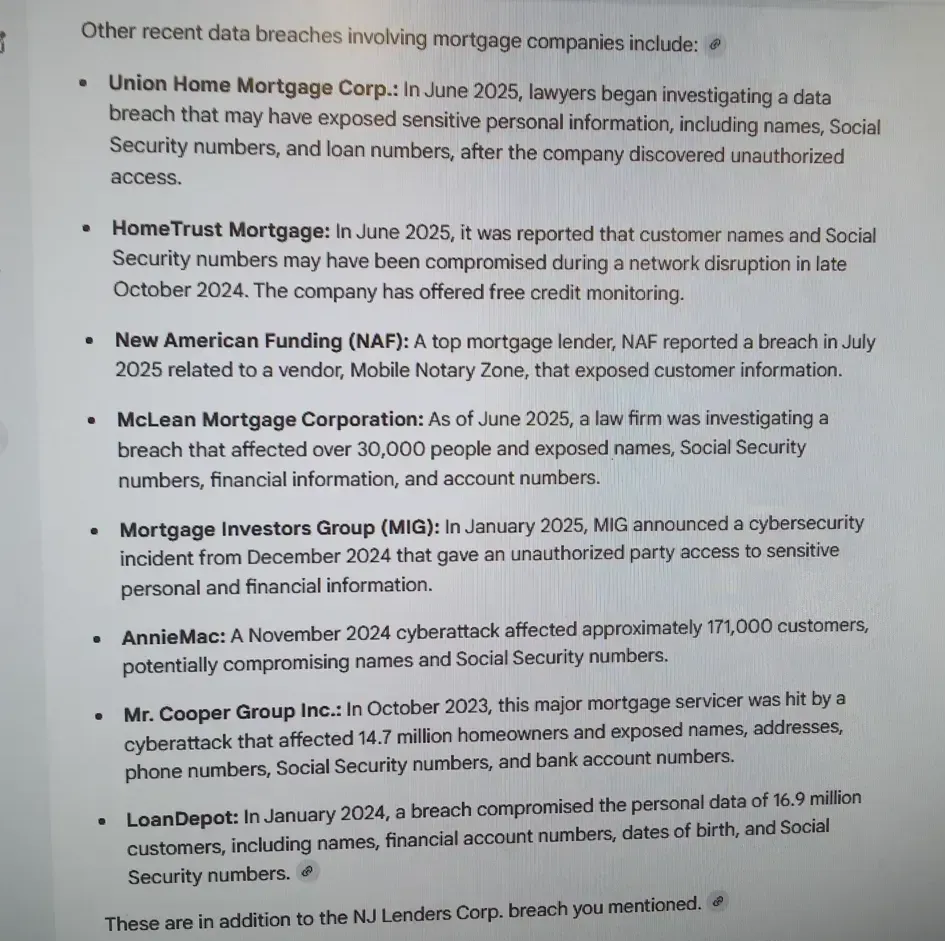

Union Home Mortgage: The Notification Failure

Breach Timeline: June 25, 2025 (discovery) Victims: 24,160+ individuals (24,160 Texas residents alone) Notification Delay: 64+ days Legal Issues: Potential state and federal law violations

Union Home Mortgage Corporation’s breach demonstrates how companies can compound the damage of a cyberattack through delayed and inadequate response.

The Attack

On June 25, 2025, the Strongsville, Ohio-based mortgage company discovered that an unauthorized third party had gained access to its network and files containing customer personal information. Despite this discovery, Union Home Mortgage waited over two months before notifying affected individuals.

The Data Compromised

The breach exposed comprehensive identity information:

- Names and Social Security numbers

- Home addresses

- Dates of birth

- Driver’s license and state identification numbers

- Passport numbers

The Notification Delay Scandal

Key Timeline:

- June 25, 2025: Breach discovered

- July 25, 2025: Reported to Massachusetts authorities (30 days later)

- August 29, 2025: Customers finally notified (65 days after discovery)

- September 12, 2025: Texas AG posted breach disclosure

This delay potentially violated multiple state notification laws, which generally require notification within 30-60 days of discovery. Several state attorneys general noted the delay in their public disclosures.

The Legal Avalanche

The notification delay triggered immediate legal action. By October 2025, five separate class action complaints had been filed against Union Home Mortgage in Ohio federal court, alleging:

- Negligence: Failure to implement adequate cybersecurity measures

- Negligence per se: Violation of FTC guidelines and data security standards

- Breach of implied contract: Violation of promises to keep customer data secure

- Unjust enrichment: Profiting from customer relationships while failing to protect their data

- Inadequate encryption: Plaintiffs claim customer data was not properly encrypted

Lead Plaintiff Victor DiMarco’s Complaint:

One lawsuit provides disturbing details about Union Home Mortgage’s alleged failures:

- Representations about taking financial privacy “very seriously” were “not matched by actual security measures”

- The company failed to adhere to commonly accepted security standards

- Failure to follow Federal Trade Commission guidance

- Placing the burden on victims to protect themselves rather than providing adequate assistance

The Company’s Size and Impact

Union Home Mortgage is a significant industry player:

- Operations in 48 states and Washington D.C.

- Approximately $5 billion in annual lending volume

- Over 1,000 employees

- 200+ branch locations

- Recent aggressive expansion including acquisition of Sierra Pacific Mortgage’s origination assets

The breach occurred during a period of growth, raising questions about whether security practices kept pace with expansion.

The Inadequate Response

The notification letters Union Home Mortgage sent to victims were criticized as “woefully inadequate” by plaintiffs’ attorneys because they:

- Failed to identify who was behind the attack

- Provided no details on how the breach occurred

- Offered no specific plans to prevent future incidents

- Initially appeared to not include credit monitoring services (though CEO Joe Panebianco later claimed they did)

- Placed responsibility on victims to “remain vigilant”

Current Status

As of October 2025:

- Multiple class action lawsuits remain pending in Ohio federal courts

- Plaintiffs are seeking to consolidate their claims

- Damages sought exceed $5 million

- No settlement discussions have been publicly disclosed

- The company continues operating but faces significant reputational damage

AnnieMac: The Three-Month Cover-Up

Breach Timeline: August 21-23, 2024 Detection: August 23, 2024 Victims: 171,074 customers Notification Date: November 14, 2024 Delay: 83 days (nearly 3 months)

American Neighborhood Mortgage Acceptance Company (doing business as AnnieMac Home Mortgage) committed one of the most egregious notification failures in recent mortgage industry history—discovering a breach in August but remaining silent until November.

The Attack

Between August 21-23, 2024, an unknown actor gained access to AnnieMac’s network systems and “viewed and/or copied certain files.” The company detected suspicious activity on August 23, 2024—the final day of the breach—suggesting the attackers were inside the system for at least two full days before detection.

The Compromised Data

The stolen information included:

- Full names

- Social Security numbers

While “only” two data elements were compromised, this combination is sufficient for comprehensive identity theft, fraudulent loan applications, tax fraud, and a host of other criminal activities.

The Inexcusable Delay

Timeline of Silence:

- August 23, 2024: Breach detected, suspicious activity identified

- October 15, 2024: Investigation presumably completed (53 days later)

- November 14, 2024: Customers finally notified via Maine AG filing (83 days after detection)

- November 14, 2024: Breach notification letters begin mailing

For nearly three months, 171,074 customers had no idea their Social Security numbers and names were in criminal hands. During this time, they:

- Continued normal financial activities

- Had no reason to monitor credit reports more closely

- Took no protective measures like credit freezes

- Remained vulnerable to tax fraud season (which begins in January)

The Legal Violations

Multiple law firms investigating the breach noted that the delay “may have violated state and federal laws.” Most state breach notification laws require notification within 30-60 days of discovery. AnnieMac’s 83-day delay significantly exceeded these thresholds.

Schubert Jonckheer & Kolbe LLP, one of several firms investigating the breach, stated: “Although the data breach occurred between August 21-23, 2024, AnnieMac did not notify its customers until approximately three months later, which may have violated state and federal laws.”

The Class Action Lawsuit

Franklin Montenegro, a current AnnieMac customer, filed a federal class action lawsuit in New Jersey court alleging:

Core Allegations:

- AnnieMac “was obligated to implement reasonable measures to prevent and detect cyberattacks”

- The company failed to adequately protect customer information

- Negligence in cybersecurity practices

- Breach of implied contract

- Breach of fiduciary duty

Claimed Damages:

- Loss of value of personal information

- Loss of time dealing with the breach

- Imminent threat and actual theft of personal information

- Financial losses from purchasing protective measures

- Increased risk of identity theft and fraud

- Invasion of privacy

- Lost value of private information

- Continued risk to private information

The Notification Letter Controversy

AnnieMac’s notification letters became a flashpoint in the lawsuit. Plaintiffs argued the letters were inadequate because they:

- Failed to identify the attackers

- Provided no details about how the breach occurred

- Offered no specific plans to prevent future incidents

- Placed burden on victims to “remain vigilant by reviewing account statements and credit reports closely”

The lawsuit specifically called out this language as “remarkable” in its attempt to shift responsibility to victims rather than the company that failed to protect their data.

The Company’s Defense

AnnieMac CEO Joe Panebianco issued statements claiming:

- The company “moved quickly to investigate and respond to the incident”

- They “assessed the security of its systems”

- They “implemented additional administrative and technical safeguards”

- They are offering one year of complimentary credit monitoring through CyEx

However, critics note that “moving quickly” apparently meant an 83-day investigation before notifying victims.

Company Context

AnnieMac is a significant mortgage lender:

- Founded in 2011, headquartered in Mount Laurel, New Jersey

- $2.5 billion in mortgage originations (last 12 months)

- 52% conventional loans, 75% purchase loans

- 447 sponsored loan officers

- 74 active branches

- Approved seller/servicer with Fannie Mae, Freddie Mac, and Ginnie Mae

- Recent expansion through acquisitions (Family First Funding in 2023, OVM Financial in 2022)

The breach occurred during a period of growth and expansion—once again raising questions about whether security infrastructure kept pace with business development.

Current Status

As of October 2025:

- Federal class action lawsuit pending in New Jersey

- Multiple law firms continuing investigations

- No settlement discussions publicly disclosed

- Company continues operations but with reputational damage

HomeTrust Mortgage: Lightning Strikes Twice

2024 Breach:

- Breach Date: October 8, 2024

- Detection: April 14, 2025 (6 months later)

- Victims: 2,234 individuals

- Notification: June 16, 2025

2022 Breach (for context):

- Breach Date: July 15, 2022

- Type: Ransomware attack

- Victims: ~17,000 individuals

- Settlement: Class action settled with compensation

HomeTrust Mortgage Company represents a disturbing pattern: a company that suffered a significant breach, presumably learned lessons, implemented improvements—and then got breached again just two years later.

The 2022 Ransomware Attack

In July 2022, Houston-based HomeTrust Mortgage first learned it was vulnerable when hackers deployed ransomware across its systems. The attack:

- Locked critical files with encryption

- Exfiltrated data including names, addresses, and Social Security numbers

- Affected approximately 17,000 borrowers, co-borrowers, and employees

- Generated significant negative publicity

HomeTrust CEO William Knapp told National Mortgage News at the time: “We’ve handled this promptly, professionally, jumped right on it, and we’re pretty sure it’s a minor event and it mitigated any damages that could be out there.”

The 2022 Class Action Settlement

Victims filed a class action lawsuit (Yuan v. HomeTrust Mortgage Co.) alleging the company:

- Failed to implement reasonable cybersecurity measures

- Should have prevented the breach through proper security protocols

- Caused financial and emotional harm to victims

HomeTrust settled without admitting wrongdoing, agreeing to:

- Undisclosed settlement fund amount

- Reimbursement for data breach-related economic damages (no cap listed)

- Lost time compensation up to 10 hours at $40/hour (maximum $400)

- Cash payments of $50 for those without economic losses

- One year of free credit monitoring through Equifax

- Final approval hearing: November 17, 2023

The 2024 Breach: History Repeats

Just one year after settling the previous breach lawsuit, HomeTrust was breached again:

October 8, 2024: External system breach due to hacking

April 14, 2025: Breach discovered (6 months later)—suggesting the attackers had unfettered access to systems for half a year

June 16, 2025: Affected individuals formally notified in writing

The 2,234 victims in the 2024 breach were likely wondering: What did HomeTrust learn from 2022? What security improvements were actually implemented? How could this happen again?

The Detection Failure

The six-month gap between the actual breach (October 2024) and detection (April 2025) is particularly alarming. This suggests:

- Inadequate intrusion detection systems

- Lack of real-time security monitoring

- Insufficient log analysis

- No anomaly detection in place

- Failure to implement lessons from 2022 breach

The Pattern of Failure

HomeTrust’s repeat breach raises troubling questions about the mortgage industry’s approach to cybersecurity:

- Are settlements just business costs? Does paying off victims replace actually fixing security?

- Is regulatory oversight sufficient? Why wasn’t HomeTrust required to demonstrate security improvements after 2022?

- What happened to the settlement money earmarked for improvements? Did those changes actually occur?

- Who verifies security claims? When companies say they’ve “enhanced security,” who checks?

Current Status

As of October 2025:

- 2,234 victims have been notified

- Identity theft protection services offered

- No class action lawsuit has been publicly filed yet for the 2024 breach

- Company continues operations across 13 locations in 8 states

NJ Lenders Corp: The Most Recent Victim

Breach Timeline: August 18, 2025 Detection: August 18, 2025 Victims: At least 599 Massachusetts residents confirmed, total number undisclosed Investigation Completed: September 12, 2025 Notifications Began: October 10, 2025

As the most recent breach in our investigation, NJ Lenders Corp demonstrates that the mortgage industry’s vulnerabilities remain unresolved even in late 2025.

The Company

NJ Lenders Corp is a substantial player in the mortgage industry:

- Founded in 1991, headquartered in Little Falls, New Jersey

- Licensed to lend in 22 states including New Jersey, New York, Massachusetts, Florida

- Over 180 employees

- Funded 100,000+ loans totaling $40+ billion

- Several brick-and-mortar locations

- Handles majority of mortgage processing in-house

The Attack

On August 18, 2025, an unauthorized party accessed certain systems in NJ Lenders’ network environment. The company appears to have detected the breach the same day—a faster response than many victims manage.

NJ Lenders immediately:

- Engaged external cybersecurity professionals

- Conducted internal review of data at risk

- Launched forensic investigation

By September 12, 2025 (25 days later), the investigation confirmed that personal information had been potentially compromised.

The Compromised Data

The breach exposed multiple data elements:

- Names

- Social Security numbers

- Driver’s license numbers

- Credit card numbers

- Debit card numbers

This combination provides criminals with everything needed for:

- Identity theft

- Fraudulent credit applications

- Unauthorized financial transactions

- Tax fraud

- Account takeovers

The Notification Process

Timeline:

- August 18, 2025: Breach occurred and detected

- September 12, 2025: Investigation confirmed compromise

- October 10, 2025: Customer notifications began (53 days after breach)

- October 20, 2025: Maine and Massachusetts AGs notified

- October 21, 2025: Vermont AG notified

The 53-day delay, while shorter than some companies, still pushed the boundaries of state notification requirements.

The Scale Mystery

As of October 2025, NJ Lenders has not disclosed the total number of affected individuals. State AG filings reveal:

- 599 Massachusetts residents affected

- 17 Maine residents affected

- Unknown Vermont residents affected

Based on the company’s 22-state footprint and 100,000+ funded loans over its 34-year history, the total victim count could be significantly higher.

The Legal Response

Multiple prominent data breach law firms have launched investigations:

Chimicles Schwartz Kriner & Donaldson-Smith LLP stated: “The exposure of sensitive Personally Identifiable Information (PII), particularly names paired with Social Security numbers, places affected individuals at a significant and ongoing risk of [identity theft].”

Barnow and Associates, P.C. noted the breach is under investigation for potential class action, highlighting NJ Lenders’ “inadequate cybersecurity measures.”

ClassAction.org opened investigation, seeking affected individuals to contact them for potential legal action.

Strauss Borrelli PLLC launched investigation, offering free consultations to victims.

The level of immediate legal interest suggests attorneys believe they have a strong case regarding NJ Lenders’ security practices.

The Response

NJ Lenders is offering affected individuals:

- Free IDX identity theft protection services

- Enrollment deadline: January 10, 2026

- Credit monitoring services

- Identity restoration services

Current Status

As of October 2025:

- Investigation remains ongoing

- Full victim count unknown

- Multiple law firms investigating potential class actions

- No lawsuits filed yet

- Company continues operations

The Common Threads: What These Breaches Reveal

When examining nine major mortgage breaches affecting 47+ million Americans, disturbing patterns emerge that suggest systemic industry-wide failures rather than isolated incidents.

1. Ransomware as the Weapon of Choice

Black Basta’s Campaign: The same ransomware gang successfully attacked both McLean Mortgage (October 2024) and Mortgage Investors Group (December 2024) within two months, suggesting:

- Systematic targeting of the mortgage sector

- Exploitation of common vulnerabilities across similar institutions

- Shared security weaknesses industry-wide

- Successful ransomware-as-a-service business model

ALPHV/BlackCat’s Sophistication: The LoanDepot attack demonstrated advanced capabilities:

- Multi-day persistent access (January 3-5, 2024)

- Data exfiltration combined with encryption

- 16.9 million victim records stolen

- Public claiming of responsibility

- Federal law enforcement’s $10 million bounty for gang leaders

2. The Data Retention Problem

Mr. Cooper’s Historical Data Nightmare: Customers who paid off mortgages in 2005-2010 (15-20 years ago) found themselves victims of the 2023 breach. This reveals:

- No data retention policies or inadequate enforcement

- Failure to archive or delete old customer data

- Indefinite storage of Social Security numbers without business justification

- Expansion of breach impact by 10+ million unnecessary victims

Industry-Wide Issue: Multiple breaches affected “former customers” going back decades:

- LoanDepot: People who “never heard of” the company

- HomeTrust: Two breaches over 2+ years

- Union Home Mortgage: Historical customer records

- AnnieMac: Long-term customer database

The Math: If companies properly deleted customer data 7 years after final business transaction (a reasonable standard), breach victim counts could be reduced by 40-60%.

3. The Notification Delay Epidemic

Average Delay: 60-80 Days

- AnnieMac: 83 days (August 23 → November 14)

- Union Home Mortgage: 65 days (June 25 → August 29)

- NJ Lenders: 53 days (August 18 → October 10)

- HomeTrust: 188 days (October 8, 2024 → April 14, 2025 discovery alone)

- McLean Mortgage: 237 days (October 17, 2024 → June 11, 2025)

Legal Standard: Most state laws require 30-60 day notifications.

The Impact: During notification delays, victims:

- Continue normal financial activities unaware of compromise

- Don’t monitor credit reports for suspicious activity

- Don’t place fraud alerts or security freezes

- Remain vulnerable to tax fraud (especially if breach occurs before tax season)

- Can’t take protective measures against identity theft

Why the Delays?

- Extended forensic investigations

- Determining scope of compromised data

- Identifying affected individuals

- Legal review and consultation

- Public relations strategizing

- Potential ransom negotiations (unconfirmed but suspected)

4. Third-Party Vulnerabilities: The Weakest Link

The Mobile Notary Zone Disaster:

New American Funding’s systems were never compromised—yet thousands of customers were affected through a vendor breach. This highlights:

Supply Chain Security Failures:

- Inadequate vendor due diligence

- No security audits of third-party providers

- Lack of contractual security requirements

- Insufficient monitoring of vendor practices

- No contingency plans for vendor breaches

The Multiplication Effect: When MNZ was breached, it potentially affected:

- Multiple mortgage lenders using their services

- Payroll providers

- Other real estate industry partners

- Unknown number of total victims

- Downstream data exposure through criminal resale

Industry Wake-Up Call: The California League of Independent Notaries issued urgent guidance, but questions remain:

- How many other mortgage lenders use vulnerable third-party services?

- Who audits the security practices of notary services, title companies, appraisers?

- What contractual protections exist for consumer data?

- Who is liable when third-party vendors are breached?

5. Inadequate Security Investment

The Evidence:

- HomeTrust breached twice in 2 years → Settlement money didn’t translate to security

- Union Home Mortgage’s unencrypted data (alleged) → Basic security measure absent

- Six-month detection failures (HomeTrust 2024) → No real-time monitoring

- $25-27 million response costs (Mr. Cooper, LoanDepot) → More expensive than prevention

- Repeat targeting by same gang (Black Basta) → Exploiting known vulnerabilities

Prevention Cost vs. Breach Cost:

Average industry security investment: $1-5 million annually Average breach costs: $25-86 million per incident

The Math: For every dollar not spent on prevention, companies pay $10-50 in breach response.

6. The Settlement Pattern: Making Victims Whole?

LoanDepot Settlement: $86.6 Million

- 16.9 million victims = $5.12 per victim

- California residents: +$14.90-$149.04 (CCPA provisions)

- Out-of-pocket reimbursement: Up to $5,000 (with documentation)

- Two years credit monitoring

Victims’ True Costs:

- Time spent dealing with breach: Unpaid

- Stress and anxiety: Uncompensated

- Credit score damage: Not covered

- Years of increased fraud risk: Ongoing

- Lost opportunities (credit denials during fraud): Not addressed

The Justice Gap: Average settlement payment ($5-50) doesn’t reflect:

- True cost of identity theft (avg. $1,500-$5,000 to resolve)

- Years of increased fraud vulnerability

- Emotional distress and time investment

- Potential credit damage lasting 7+ years

7. Regulatory Inadequacy

No Federal Breach Notification Standard:

- 50 states have 50 different laws

- Inconsistent requirements for timing and disclosure

- No uniform penalties for violations

- Easy for companies to exploit weakest standards

No Security Standards Enforcement:

- FTC guidelines are recommendations, not requirements

- No mandatory security audits

- No certification requirements

- No consequences for inadequate security until after breach

No Data Retention Limits:

- Companies can keep customer data indefinitely

- No requirement to delete old records

- Victims from decades ago unnecessarily exposed

- Expansion of breach impact through poor data hygiene

8. The Dark Web Threat

Post-Breach Reality:

Multiple companies claim to be “monitoring the dark web” with “no evidence” of data misuse. However:

Dark Web Economics:

- SSN + Name + DOB package: $1-10 on dark web markets

- Full financial profile: $50-200

- Mortgage application data: $100-500 (includes full financial history)

The Timeline:

- Data typically appears on dark web 3-6 months post-breach

- Initial sales to “premium” buyers

- Later public release if ransom not paid

- Years of availability for purchase

- Multiple resales through criminal networks

What “No Evidence of Misuse” Really Means:

- No reported cases of fraud…yet

- No public listings…that we’ve found

- No victim complaints…so far

- Criminals haven’t been caught…yet

Reality: Data stolen in breaches can surface years later, making “no evidence” claims premature.

9. Repeat Offenders Face No Additional Consequences

HomeTrust: Breached 2022 → Settled lawsuit → Breached again 2024

Why no additional penalties for repeat failures?

- No “repeat offender” provisions in breach laws

- Settlements don’t require proven security improvements

- No ongoing oversight or auditing

- Companies can pay off victims instead of fixing security

The Incentive Problem:

- Cost of lawsuit settlement: $1-10 million

- Cost of comprehensive security overhaul: $5-20 million

- Rational choice: Settle and hope for no future breach

The Human Cost: Beyond the Statistics

While 47+ million victims is a staggering number, it’s important to understand what these breaches mean for actual people:

Real Victim Experiences (from public forums and reports):

The “I’ve Never Heard of Them” Victims: Hundreds of LoanDepot breach victims reported never having business with the company:

- “I’ve never had a mortgage, never applied for one, and never even heard of LD”

- Data obtained through unknown third-party relationships

- No idea how company obtained their information

- Anger at being victimized by companies they never chose to trust

The “It’s Been Decades” Victims: Mr. Cooper victims from 2001-2005:

- “Last mortgage was 2005, paid off in 2010”

- “Why are they still storing my SSN after 15-19 years?”

- “I haven’t been their customer for almost two decades”

- Outrage that companies never deleted their data

The Multiple Victim Problem: Given overlap in the industry, many people were breached multiple times:

- Active mortgage customers in 2023 likely affected by Mr. Cooper

- Refinanced in 2024 might hit LoanDepot

- New home purchase in 2025 could involve Union Home or NAF

- Same person potentially affected 3+ times with different SSN exposures

The Credit Consequence: Victims report:

- Unexpected credit denials during fraud review

- Lower credit scores from fraud alerts

- Increased scrutiny on legitimate applications

- Lost opportunities (apartment rentals, employment, etc.)

- Years of “explaining” their breach status

The Emotional Toll

Immediate Reactions:

- Violation of trust

- Anger at companies’ security failures

- Fear of identity theft

- Helplessness and lack of control

Long-term Impacts:

- Constant vigilance monitoring accounts

- Anxiety when applying for credit

- Hesitation to conduct financial transactions

- Loss of faith in financial institutions

- Chronic stress from unresolved threat

The Time Investment:

- Reading and understanding breach notice: 30-60 minutes

- Enrolling in credit monitoring: 1-2 hours

- Setting up fraud alerts: 1-2 hours per bureau

- Freezing credit reports: 2-3 hours

- Monitoring accounts regularly: 1-2 hours monthly ongoing

- Total: 15-20+ hours of unpaid victim labor

The Financial Reality

Compensated Costs:

- Credit monitoring provided by company

- Settlement payments: $5-70 per victim

- Out-of-pocket reimbursement: Up to $5,000 (with extensive documentation)

Uncompensated Costs:

- Time investment (15-20 hours at even minimum wage = $200-300)

- Stress and mental health impact

- Credit score reduction

- Lost financial opportunities

- Ongoing monitoring costs after free period ends

- Identity theft resolution if fraud occurs (avg. $1,500-5,000)

Industry Response: Too Little, Too Late?

What Companies Are Promising

Most breach notifications include generic promises:

- “Taking this matter very seriously”

- “Implementing additional safeguards”

- “Enhanced security measures”

- “Working with cybersecurity experts”

- “Improving monitoring and detection”

What Rarely Changes

Structural Problems Persist:

- Same vulnerability to ransomware

- Continued indefinite data retention

- Third-party vendor risks unaddressed

- Notification delays continue

- Detection capabilities remain inadequate

The Settlement Pattern

LoanDepot’s $9.34 Million in “Business Improvements”:

- Enhanced data management

- Increased cloud security

- Better threat detection capabilities

Questions:

- Why weren’t these measures in place before?

- Who verifies these improvements actually happen?

- What independent audit confirms effectiveness?

- How long before the company is breached again?

The Credit Monitoring Band-Aid

Every breach response includes:

- 1-2 years free credit monitoring

- Identity theft insurance

- Fraud consultation services

Why This Isn’t Enough:

- Identity theft risk lasts 7+ years (life of credit report)

- Criminals often wait 2-3 years to use stolen data (after free monitoring expires)

- Credit monitoring is reactive, not preventive

- Doesn’t address non-credit identity theft (medical, employment, tax fraud)

- Victims still must invest significant time and effort

What Meaningful Response Would Look Like

1. Mandatory Security Standards:

- Annual third-party security audits

- Required encryption of all sensitive data

- Mandatory intrusion detection systems

- Real-time security monitoring

- Vendor security requirements and audits

2. Data Retention Limits:

- Maximum 7-year retention after business relationship ends

- Annual data cleanup audits

- Penalties for retaining unnecessary data

- Customer right to demand deletion

3. Notification Requirements:

- Maximum 30 days from detection

- Complete disclosure of breach details

- Specific information on what went wrong

- Clear description of measures to prevent recurrence

4. Meaningful Accountability:

- Increased penalties for repeat breaches

- Personal liability for executives

- Mandatory security improvements before continuing operations

- Independent verification of improvements

5. Victim-Centered Compensation:

- Lifetime credit monitoring (not 1-2 years)

- Automatic compensation for time investment

- Pre-approved fraud resolution services

- No-documentation reimbursement for fraud losses

The Regulatory Failure

Patchwork State Laws

The Problem:

- 50 states, 50 different breach notification laws

- Inconsistent timing requirements (30-90 days)

- Varying disclosure requirements

- Different definitions of “personal information”

- No uniform penalties

The Loophole: Companies can:

- Comply with weakest state standards

- Forum shop for most favorable courts

- Exploit inconsistencies between jurisdictions

- Face minimal penalties in some states

No Federal Breach Standard

What’s Missing:

- Uniform national breach notification law

- Consistent timing requirements

- Standard disclosure obligations

- Clear penalty structure

- Federal enforcement mechanism

Legislative Efforts: Multiple federal breach notification bills introduced over past decade—none passed.

Why?

- Industry lobbying against strict standards

- State rights concerns

- Lack of political will

- Complexity of creating uniform standard

Inadequate Security Requirements

Current Reality:

- FTC provides “guidelines” (not requirements)

- No mandatory security standards for mortgage companies

- No certification or licensing based on security

- No regular security audits required

- No consequences until after breach occurs

What’s Needed:

- Mandatory minimum security standards

- Regular independent security audits

- Certification requirements for handling financial data

- Annual security disclosures to regulators

- Proactive enforcement before breaches occur

The Enforcement Gap

After Breach Occurs:

- State AG investigations (sometimes)

- FTC enforcement action (rarely)

- Class action lawsuits (usually settled without admission)

- Modest fines relative to company revenue

What’s Missing:

- Criminal prosecution of negligent security practices

- Personal liability for executives

- Revocation of licenses for repeat offenders

- Punitive damages for egregious failures

- Mandatory security improvements before continuing operations

The Vendor Problem

No Oversight of Third-Parties:

- Mobile Notary Zone breach affected multiple companies

- No security standards for vendors handling consumer data

- No audit requirements

- No certification processes

- Unclear liability when vendors are breached

What’s Needed:

- Security standards for all vendors handling consumer data

- Mandatory security audits of third-parties

- Clear liability framework

- Contractual security requirements

- Industry certification programs

What Consumers Can Do (While We Wait for Real Solutions)

While systemic change is needed, individuals affected by these breaches must take immediate protective action.

Immediate Actions (First 48 Hours)

1. Verify the Breach Notification:

- Check notification came from legitimate company address

- Visit company website directly (don’t click email links)

- Verify breach listed on state AG websites

- Confirm with company directly via phone

2. Document Everything:

- Save all breach notification letters

- Screenshot emails and online notices

- Keep timeline of all correspondence

- Note all time spent responding (for potential claims)

3. Enroll in Offered Services:

- Credit monitoring (even if already have it)

- Identity theft insurance

- Fraud consultation services

- Use provided enrollment codes before expiration

Week 1 Actions

1. Place Fraud Alerts: Contact one of three credit bureaus (they’ll notify the others):

- Equifax: 1-888-766-0008

- Experian: 1-888-397-3742

- TransUnion: 1-800-680-7289

Initial fraud alerts last 1 year (free), force creditors to verify identity.

2. Request Free Credit Reports: Visit AnnualCreditReport.com (only official source)

- Entitled to one free report per bureau annually

- After breach, can request additional reports

- Review carefully for accounts you didn’t open

- Check for address changes you didn’t make

3. Consider Credit Freeze: More protective than fraud alert:

- Prevents new accounts from being opened

- Must unfreeze temporarily when you apply for credit

- Free to freeze and unfreeze

- Recommended for children and elderly parents

Contact Same Three Bureaus to Freeze:

- Equifax: equifax.com/personal/credit-report-services

- Experian: experian.com/freeze

- TransUnion: transunion.com/credit-freeze

4. File with FTC: Report identity theft at IdentityTheft.gov:

- Creates official record

- Generates recovery plan

- Provides affidavit for creditors

- Helps with law enforcement reports

First Month Actions

1. Monitor All Financial Accounts:

- Check bank accounts daily

- Review credit card transactions weekly

- Watch for small “test” charges (pennies or dollars)

- Report suspicious activity immediately

2. Secure Your Accounts:

- Change passwords on all financial accounts

- Use unique password for each account (password manager recommended)

- Enable two-factor authentication everywhere available

- Update security questions to non-public answers

3. File Taxes Early: One of the most common uses of stolen SSN:

- File tax return as early as possible (January)

- Prevents criminals filing fraudulent returns first

- Consider IRS Identity Protection PIN (IP PIN)

4. Monitor Credit Reports:

- Set calendar reminders to check monthly

- Rotate between three bureaus (every 4 months)

- Look for hard inquiries you didn’t authorize

- Check for new accounts or credit lines

Ongoing Protection (Months 2-12+)

1. Stay Vigilant:

- Continue monitoring all accounts

- Don’t assume threat is over after free monitoring expires

- Criminals often wait 2-3 years to use stolen data

- Consider paying for ongoing monitoring after free period

2. Respond to Any Signs of Fraud Immediately:

- Report suspicious charges within 60 days

- File police reports for identity theft

- Contact creditors’ fraud departments

- Use FTC identity theft report

3. Document All Breach-Related Expenses: For potential class action claims:

- Keep receipts for credit monitoring after free period

- Log time spent responding (hours, activities)

- Document any fraud incidents and resolution efforts

- Save communications with creditors, companies, law enforcement

4. Consider Additional Protection:

- Identity theft insurance (if not provided)

- Lifelock or similar services (after free monitoring expires)

- Regular credit monitoring

- Annual comprehensive identity audit

Special Considerations

If Your Child’s Data Was Breached:

- Request credit freeze for minor (legal guardian required)

- Check if child already has credit file (shouldn’t unless fraud occurred)

- Monitor for signs of child identity theft

- Consider credit monitoring when child approaches 16

If You’re Elderly or Caretaking:

- Set up joint alerts on accounts

- Give trusted person monitoring access

- Consider power of attorney for fraud response

- Watch for elder-specific scams using stolen data

If You’re a Mortgage Customer:

- Watch for fake mortgage modification scams

- Verify any communications about your loan

- Be skeptical of “urgent” payment requests

- Contact servicer directly via known phone number

What Regulators Should Do (But Probably Won’t)

Based on analysis of these nine major breaches, here are specific policy recommendations:

1. Federal Breach Notification Standard

Requirement:

- Maximum 30 days notification from detection

- Standardized content requirements

- Direct notification to regulators within 72 hours

- Public disclosure on company website

- Details about nature of breach (not generic statements)

Penalties:

- $1,000 per day per affected individual for delayed notification

- Criminal liability for executives who intentionally delay

- Mandatory external audit before resuming operations

2. Mandatory Security Standards

Requirements:

- Annual independent security audits

- Encryption of all sensitive data at rest and in transit

- Real-time intrusion detection systems

- Security Operations Center (SOC) monitoring

- Vendor security assessment and audits

- Incident response plan (tested annually)

Enforcement:

- License contingent on security certification

- Surprise security audits by regulators

- Public disclosure of security audit results

- Mandatory improvements before continuing operations

3. Data Retention Limits

Requirements:

- Maximum 7-year retention after business relationship ends

- Annual data cleanup audits

- Consumer right to request deletion

- Penalties for retaining unnecessary data

- Increased liability for breaches of old data

Enforcement:

- Data retention audits as part of regulatory oversight

- Fines for unnecessary data retention

- Increased damages in breaches involving old data

- Criminal liability for willful retention violations

4. Third-Party Vendor Standards

Requirements:

- Security standards for all vendors handling consumer data

- Mandatory vendor security audits

- Clear contractual liability framework

- Industry certification programs

- Direct vendor notification to regulators

Enforcement:

- Lender liable for vendor breaches (encourages due diligence)

- Vendor registration and certification

- Public database of certified vendors

- Penalties for using uncertified vendors

5. Meaningful Victim Compensation

Requirements:

- Minimum $200 automatic payment per victim (time compensation)

- Lifetime credit monitoring (not 1-2 years)

- No-documentation reimbursement up to $10,000 for fraud

- Automatic fraud resolution services

- Mental health services coverage

Enforcement:

- Compensation fund established before operations resume

- Escrowed funds for victim compensation

- Independent administrator for claims

- No settlement required for basic compensation

6. Repeat Offender Provisions

Requirements:

- Doubled penalties for second breach within 5 years

- Mandatory security overhaul for repeat breaches

- Personal liability for executives in repeat breaches

- Potential license revocation for multiple failures

- Public “repeat offender” designation

Enforcement:

- Database tracking company breach history

- Escalating regulatory oversight

- Criminal prosecution for gross negligence

- Board member liability for oversight failures

7. Criminal Liability for Negligence

Create New Federal Crime:

- “Negligent Data Security Resulting in Breach” Criminal liability for executives who:

- Knowingly underfund security

- Ignore security recommendations

- Fail to implement basic protections

- Prioritize profits over security

Penalties:

- Up to 5 years prison for first offense

- Up to 10 years for breaches affecting 1+ million

- Personal fines up to $1 million

- Ban from serving as executive in data-handling companies

The Path Forward: What Change Looks Like

Short-Term (1-2 Years)

Industry Self-Regulation Attempts:

- Trade associations create voluntary standards

- Sharing of threat intelligence

- Best practices documentation

- Industry-funded security audits

Likely Outcome: Insufficient without regulatory teeth.

State-Level Action:

- More states pass comprehensive breach laws

- California-style consumer privacy laws expand

- States compete for strictest standards

- Continued patchwork of requirements

Likely Outcome: Helpful but inconsistent.

Class Action Settlements:

- More mortgage breach lawsuits

- Larger settlements (following LoanDepot’s $86.6M)

- Standard compensation frameworks emerge

- Precedent for meaningful victim compensation

Likely Outcome: Creates financial incentive for security.

Medium-Term (3-5 Years)

Federal Legislation:

- National breach notification standard

- Basic security requirements

- Data retention limits

- Vendor oversight framework

Likelihood: Moderate (depends on political climate and major incidents).

Insurance Market Response:

- Cyber insurance requirements increase

- Insurers mandate security standards

- Premium pricing based on security posture

- Coverage denial for repeat offenders

Likely Outcome: Market-driven security improvements.

Technology Solutions:

- AI-powered threat detection becomes standard

- Zero-trust architectures widely adopted

- Automated compliance monitoring

- Blockchain-based audit trails

Likely Outcome: Reduces but doesn’t eliminate breaches.

Long-Term (5-10 Years)

Cultural Shift:

- Security becomes competitive advantage

- Companies advertise security certifications

- Consumer choice driven by security reputation

- Industry-wide security culture emerges

Likelihood: Possible if breach costs continue rising.

Regulatory Maturity:

- Comprehensive federal security standards

- Active enforcement and criminal prosecution

- Regular security audits

- Meaningful penalties for failures

Likelihood: Depends on sustained political pressure.

Technology Evolution:

- Quantum-resistant encryption

- Decentralized identity systems

- Biometric authentication ubiquitous

- AI vs. AI security arms race

Likely Outcome: New vulnerabilities emerge but detection improves.

Conclusion: 47 Million Reasons to Demand Better

The mortgage industry’s data breach epidemic isn’t a series of unfortunate accidents—it’s a predictable result of inadequate security investment, insufficient regulation, poor data hygiene, and misaligned incentives.

The Math Doesn’t Lie:

- 47+ million Americans victimized

- $150+ million in settlement and response costs

- Decades of ongoing identity theft risk

- Preventable with proper security investment

The Pattern Is Clear:

- Same vulnerabilities exploited repeatedly

- Same ransomware gangs attacking multiple targets

- Same notification delays

- Same inadequate responses

- Same lack of meaningful consequences

The Solution Requires:

- Strong federal security standards

- Meaningful penalties for failures

- Data retention limits

- Vendor oversight

- Victim-centered compensation

- Criminal liability for negligence

Until regulators, lawmakers, and industry leaders treat data security as seriously as they treat profitability, consumers will continue paying the price—not just in dollars, but in stress, time, and ongoing vulnerability to identity theft.

For the 47 million victims of these nine breaches, and the millions more who will be affected by future incidents, the message is clear: the mortgage industry has broken your trust. Whether they can rebuild it depends on actions, not promises.

What You Can Do Right Now

If You’re a Breach Victim:

- Take protective actions outlined in this article

- Document all time and expenses

- Join class action lawsuits when filed

- Submit victim impact statements to regulators

- Share your story publicly

If You’re a Consumer:

- Ask lenders about security practices before doing business

- Choose companies with strong security reputations

- Minimize sensitive data provided

- Maintain your own security best practices

- Advocate for stronger data protection laws

If You’re a Policymaker:

- Support federal breach notification legislation

- Fund regulatory oversight of financial institutions

- Create criminal penalties for security negligence

- Mandate data retention limits

- Protect whistleblowers who report security failures

If You’re Industry Leadership:

- Invest in security BEFORE breaches occur

- Implement defense-in-depth strategies

- Conduct regular third-party security audits

- Delete unnecessary customer data

- Treat security as business-critical, not cost center

The mortgage industry breach epidemic can be solved—but only with comprehensive action from all stakeholders. The 47 million victims of these nine breaches deserve better. So do the millions who will be affected by tomorrow’s breach if we fail to act today.

This investigation analyzed nine major mortgage company data breaches from October 2023 through October 2025, affecting a combined 47+ million individuals. Data sources include state attorney general breach notifications, SEC filings, court documents, company disclosures, and security research.

For updates on ongoing investigations and new breaches, follow breached.company.