When Markets "Overheat": The Suspiciously Timed CME "Cooling Failure" That Halted Silver's Historic Breakout

Executive Summary

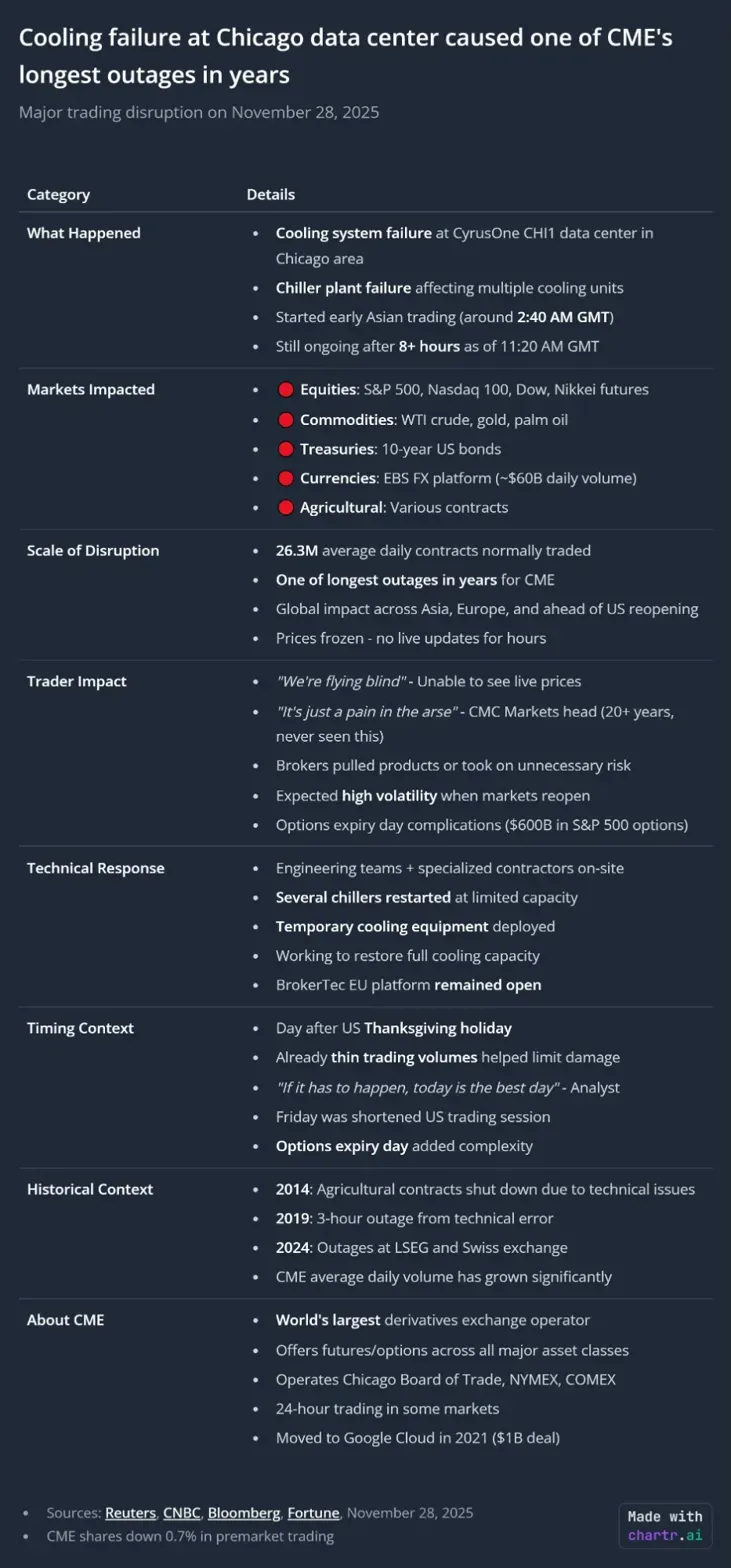

On November 28, 2025, as silver futures approached historic breakout levels above $54/oz and gold surged past $4,186, the Chicago Mercantile Exchange—the world's largest derivatives exchange—experienced a "cooling system failure" at its CyrusOne CHI1 data center in Aurora, Illinois. The 10+ hour outage halted trading across $26.3 million in daily contracts spanning equities, commodities, treasuries, currencies, and agricultural products just as precious metals threatened to breach critical resistance levels.

The timing was extraordinary: silver had gained 84% year-over-year and was poised for a breakout that would devastate short positions. Within minutes of the halt, spot silver inexplicably "nuked" $1 in over-the-counter trading despite frozen CME pricing. Gold printed two $40 liquidation wicks that instantly recovered—a pattern suggesting not organic selling but extreme plumbing stress.

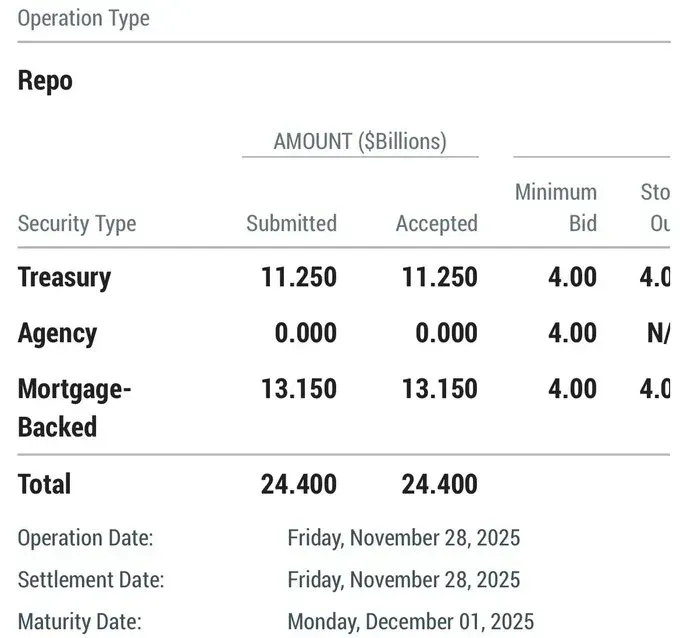

Simultaneously, banks borrowed $24.4 billion through the Federal Reserve's standing repo facility on a shortened post-Thanksgiving trading session—a massive liquidity injection that coincided with the exchange's "maintenance window."

This wasn't just a technical glitch. This was a case study in how critical financial infrastructure can fail at precisely the moment it threatens established market interests.

The Silver Squeeze Nobody Saw Coming

The Setup: A Perfect Storm for Precious Metals

In the days leading up to November 28, silver had entered an unprecedented rally:

- +84.41% year-over-year performance (trading at $56.45)

- +163% cumulative gain since late 2023

- Outpacing gold by 21 percentage points in recent months

- Trading at multi-decade highs not seen since the 1980 Hunt Brothers squeeze

The fundamentals supporting this rally were ironclad:

- Supply deficits: Industrial demand from solar, EV, and electronics sectors driving consumption beyond mine supply and recycling capacity for multiple consecutive years

- Fed pivot expectations: December rate cut anticipation weakening the dollar

- Industrial demand surge: Silver's dual role as precious metal and critical industrial commodity creating unprecedented demand pressure

- Thin holiday liquidity: Post-Thanksgiving trading volumes 25%+ below 30-day averages, amplifying volatility

Multiple major banks were scrambling to revise forecasts upward:

- UBS raised projections to $60/oz by 2026

- HSBC increased average price forecasts amid widening supply deficits

- Market analysts noted silver was trading well ahead of bank targets, forcing catch-up revisions

What Happened at the Critical Moment

As Asia markets opened on Thursday evening US time (early Friday morning in Asian markets), silver approached $54—a level that represented catastrophic exposure for short positions accumulated during years of paper market manipulation.

Traders described the pre-halt environment:

- Shanghai silver contracts set new Yuan highs, rising 2.0% to ¥12,682/kg

- London silver fixing around $53.88 matched mid-November's second-highest benchmark

- Silver futures book was "very thin" according to commodity traders

- A trade cleared the entire offer side with no quotes left

- Gold–silver ratio had compressed to 77:1, down from high-80s to low-90s

Then, at 9:44 PM ET on November 27 (2:40 AM GMT November 28), everything stopped.

CME announced via Twitter: "Due to a cooling issue at CyrusOne data centers, our markets are currently halted."

The "Cooling Issue": Deconstructing the Official Story

What CME Claims Happened

According to official statements from CME Group and CyrusOne:

CyrusOne Statement: "On November 27, our CHI1 facility experienced a chiller plant failure affecting multiple cooling units. Our engineering teams, along with specialized mechanical contractors, are on-site working to restore full cooling capacity."

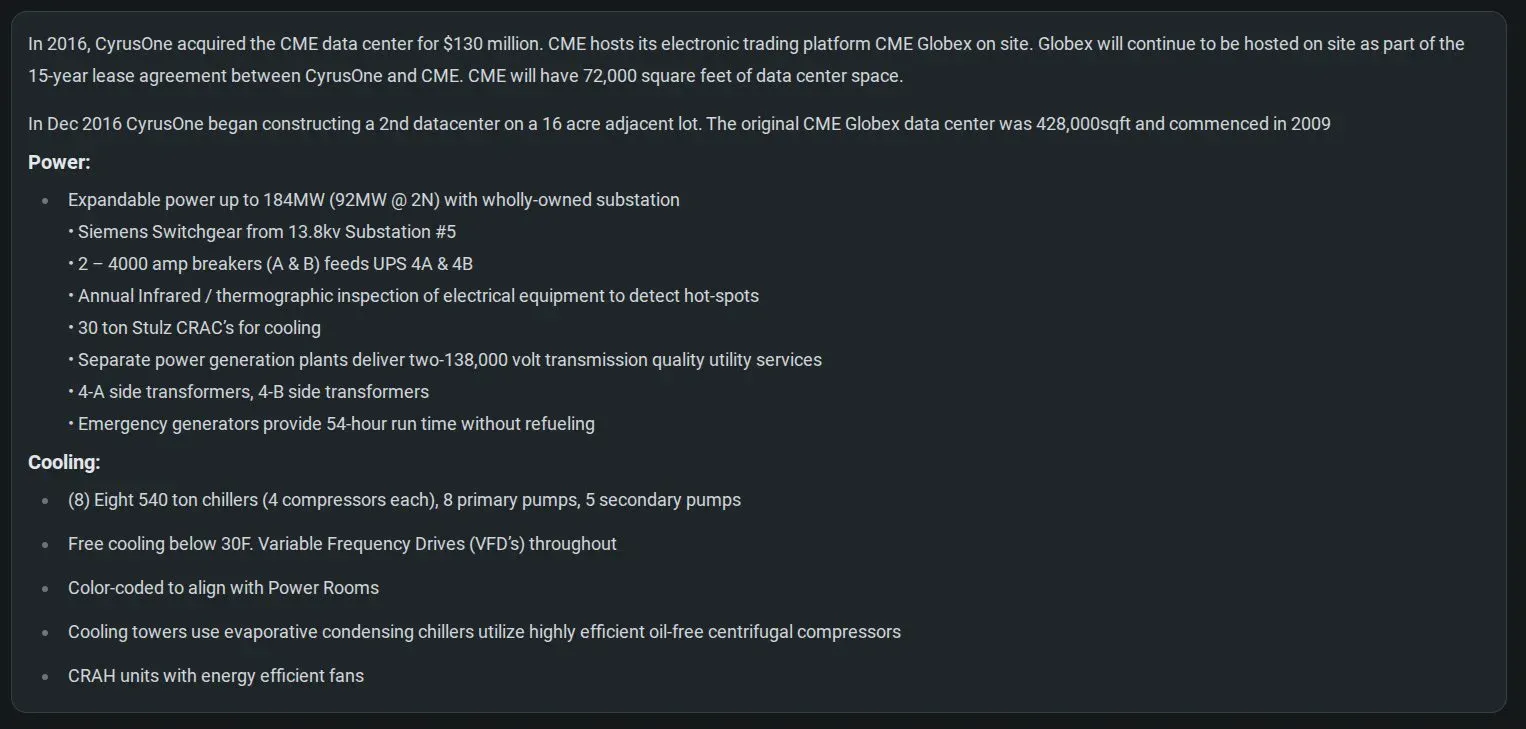

The CHI1 facility in Aurora, Illinois is part of a 450,000 sq ft campus that CME sold to CyrusOne in 2016 for $130 million in a sale-leaseback deal. The infrastructure specifications are impressive:

Power Infrastructure:

- Expandable power up to 184MW (92MW at 2N)

- Wholly-owned substation with Siemens Switchgear

- Two 4000-amp breakers feeding UPS systems

- 54-hour emergency generator runtime without refueling

- Annual infrared/thermographic inspection of electrical equipment

Cooling Infrastructure:

- Eight 540-ton chillers (4 compressors each)

- 8 primary pumps, 5 secondary pumps

- Free cooling below 30°F via Variable Frequency Drives

- Color-coded alignment with power rooms

- Evaporative condensing chillers with highly efficient oil-free centrifugal compressors

- CRAH units with energy-efficient fans

The Technical Implausibility

Here's what makes the official story suspect from an infrastructure perspective:

1. Massive Redundancy Should Have Prevented Total Failure

With 8 independent chillers, each with 4 compressors, for a total of 32 compressor units, a failure severe enough to take down the entire facility would require:

- Simultaneous failure of multiple independent cooling units

- Failure of free cooling systems (it was below 30°F in Aurora that night)

- Failure of emergency protocols designed to prevent cascade failures

- Failure of monitoring systems that should have provided advance warning

2. Weather Conditions Favored Cooling

November 27 overnight temperatures in Aurora, Illinois were in the mid-20s to low 30s Fahrenheit—perfect conditions for the facility's free cooling mode that operates below 30°F. In these conditions, the data center should have been able to cool using outside air economization with minimal chiller usage.

3. History of Infrastructure Issues at This Specific Facility

CyrusOne's Aurora campus has a documented history of serious infrastructure problems:

- April 2025: Transformer failure forced multi-day backup generator operation, causing noise complaints from neighboring residents described as "unlivable" and "horrible"

- August 2025: Additional emergency repairs requiring 8 hours of generator operation

- Community complaints led to construction of temporary and permanent sound walls

- Residents questioned whether the city was enforcing occupancy rules

The recurring infrastructure issues suggest either:

- Deferred maintenance creating systemic vulnerabilities

- Oversubscription beyond designed capacity

- Operational management failures in a facility handling one of the world's most critical financial systems

4. One Data Center, Global Systemic Risk

CME sold this facility in 2016 but remains dependent on it via a 15-year lease agreement. As one analyst noted: "CME sold it for $130M in 2016 and leased it back. They don't own the building. They don't control the cooling. 90% of global derivatives pricing now depends on pipes they sold nine years ago."

The Market Manipulation Evidence

Timing Analysis: Too Convenient to Ignore

Let's examine what happened in the hours surrounding the "cooling failure":

Pre-Halt (9:00 PM - 9:44 PM ET, November 27):

- Silver trading at $53.88-$54.00 range

- Extremely thin liquidity due to Thanksgiving holiday

- Asian session traders active, European session about to begin

- Silver futures order book described as having "no quotes left" on offer side

- Gold printing unusual $40 liquidation wicks that instantly recovered

During Halt (9:44 PM November 27 - 8:30 AM November 28 ET):

- 10 hours 46 minutes of complete trading suspension

- Over-the-counter silver markets experience $1 drop in minutes despite no CME price discovery

- Gold experiences erratic moves with bid-offer spreads 20x wider than normal

- Traders worldwide locked out, unable to adjust positions or manage risk

- Options expiry day complications ($600B in S&P 500 options)

Simultaneous Financial System Events:

- Banks borrowed $24.4 billion through Fed's standing repo facility

- $11.25 billion in Treasury securities

- $13.15 billion in mortgage-backed securities

- Total accepted: $24.4 billion (submitted and accepted were identical)

- Operation date and settlement date: Friday, November 28, 2025

- Maturity date: Monday, December 1, 2025

Post-Reopen (8:30 AM ET onwards):

- Markets gradually resume with "limited capacity" operations

- Treasury futures and SOFR options experience continued delays

- Trading volumes remain suppressed throughout shortened session

- Silver consolidates below breakout levels

Market Participant Testimony

The quotes from professional traders paint a damning picture:

Thomas Helaine (TP ICAP Europe): "It's a bit like flying dark. When you're trading cash equity like us, US futures give you an indication of where the market is going before the open."

Gnanasekar Thiagarajan (Kaleesuwari Intercontinental): "Traders sitting with a position are certainly quite angry."

One commodity trader (anonymous): "The 'glitch' excuse is bs. Silver futures book was very thin, then a trade cleared the Offer side with no quotes left. According to him CME is giving time to market makers to reposition and avoid a price print 'off the charts.'"

CMC Markets head (20+ years experience): "It's just a pain in the arse. I've never seen this." This from a veteran who has witnessed every major market event for two decades.

The Fed Repo Connection: $24.4 Billion in "Coincidental" Timing

The timing of the massive Federal Reserve repo operation cannot be overlooked:

Context: The Fed's standing repo facility (SRF) provides emergency liquidity when short-term funding markets seize up. Typical daily usage is zero to single-digit billions. The October 31, 2025 operation of $50 billion was considered extraordinary—the largest since the 2019 repo crisis.

November 28 Operation:

- $24.4 billion total across Treasury and mortgage-backed securities

- Submitted amount exactly matched accepted amount (unusual)

- Occurred during a half-day trading session (not typical month-end)

- Same day as CME "cooling failure"

- One day before December 1 maturity

The Timing Question: Why did banks need $24.4 billion in emergency liquidity on a quiet post-Thanksgiving Friday morning, precisely when the world's largest derivatives exchange was experiencing "cooling problems"?

Possible explanations:

- Margin call pressures from extreme precious metals volatility requiring emergency funding

- Dealer desks caught off-guard by holiday liquidity crisis needing Fed intervention

- Coordinated intervention to provide liquidity buffer during "planned" CME maintenance window

- Pure coincidence (least likely)

The Cybersecurity and Infrastructure Perspective

Critical Infrastructure Dependency: A CISO's Nightmare

As a cybersecurity professional with 15+ years conducting security assessments, this incident exposes catastrophic single points of failure in global financial infrastructure:

Third-Party Risk Concentration:

- CME Group (market cap ~$100 billion) depends on one data center operated by a third-party vendor

- This data center hosts 90% of global derivatives pricing

- A single cooling system failure can paralyze $26.3 million in daily contracts

- No apparent hot-standby facility capable of immediate failover

Comparison to Similar Infrastructure Failures:

Our recent analysis at breached.company documented several major infrastructure failures in 2025:

- AWS US-EAST-1 Outage (October 20, 2025): DNS resolution failure took down 1,000+ services, causing $75+ million/hour in damages. Single software bug in Virginia data center created cascading global failures.

- Microsoft Azure Front Door Outage (October 29, 2025): Inadvertent configuration change caused 12-hour outage affecting Azure, Microsoft 365, Xbox Live, and thousands of customer-facing services including Starbucks, Costco, Capital One, Alaska Airlines, and Zoom.

- Cloudflare Outage (November 2025): Single software issue in Virginia data center disrupted McDonald's kiosks, nuclear plant security systems (PADS), RuneScape, and countless critical services.

The Pattern: In each case, organizations that seemed to have robust redundancy and failover capabilities experienced catastrophic failures from single-point failures. The CME incident follows this pattern but with significantly higher financial stakes.

Operational Security Red Flags

From a physical security and operational perspective (I work event security at major venues while consulting), several aspects trouble me:

1. Insufficient Environmental Monitoring

Modern data centers should have:

- Real-time temperature monitoring at rack, row, and facility levels

- Predictive analytics identifying trending failures before they become critical

- Automated alerting with tiered escalation

- Multiple hours of advance warning before critical temperature thresholds

For a complete chiller plant failure to occur without advance warning suggests:

- Monitoring systems failed

- Alerts were ignored

- Infrastructure was already operating in degraded state

- Or this wasn't actually a chiller failure

2. Inadequate Disaster Recovery Planning

CME's incident response reveals:

- No immediate failover to backup facility

- 10+ hours to restore operations (compared to 2-4 hours for similar incidents in 2019)

- Gradual, piecemeal restoration rather than coordinated full recovery

- Treasury futures and SOFR options continued experiencing issues after main markets reopened

For an organization handling $26.3 million in daily contract volume and providing global price discovery, this represents a fundamental business continuity failure.

3. Sale-Leaseback Risk Materialization

CME's 2016 decision to sell the data center for $130 million while leasing it back created exactly the risk that materialized:

- Loss of infrastructure control: CME cannot independently verify or mandate upgrades

- Operational dependency: Reliant on CyrusOne's maintenance and staffing decisions

- Cost optimization conflicts: CyrusOne may prioritize cost reduction over redundancy

- Multi-tenant conflicts: Other CyrusOne customers at CHI1 may affect CME operations

This is a textbook third-party risk management failure—a lesson every CISO should internalize.

Historical Context: When Exchanges "Conveniently" Fail

The Pattern of Strategic Technical Failures

This is not the first time exchanges have experienced technical issues at market-critical moments:

CME Historical Outages:

- 2019: Hours-long outage due to "technical error"

- 2014: Agricultural contracts shut down due to technical issues

- 2024: Outages at LSEG and Swiss exchanges

Other Notable Exchange "Glitches":

- Robinhood (January 2021): Platform restrictions during GameStop short squeeze prevented retail traders from buying, protecting institutional short positions

- LME Nickel (March 2022): London Metal Exchange cancelled $3.9 billion in nickel trades and suspended trading when prices surged 250% in hours, devastating short positions held by major Chinese producer

- Interactive Brokers: Multiple instances of "technical issues" during high volatility periods

The Common Thread: Technical failures disproportionately occur when markets threaten to move in directions that would devastate institutional positions or expose structural market vulnerabilities.

The Terry Duffy Bribery Controversy

CME CEO Terry Duffy appeared on Fox News in November 2022 to discuss the FTX collapse. During the interview, he made a statement that raised eyebrows:

Tucker Carlson asked where SEC chairman Gary Gensler was during FTX's mismanagement. Duffy responded: "I don't know where Gary Gensler was, but my regulator at the CTFC I bribe, I asked them, why in the world are you invoking the Commodity Exchange Act?"

While Duffy may have misspoken or meant "brief" instead of "bribe," the statement has never been clarified or corrected over three years later. For the head of the world's largest derivatives exchange to casually mention bribing regulators—even potentially in jest—reveals a comfort level with regulatory capture that should concern market participants.

The Technical Analysis: What Really Happened

Silver Market Mechanics During the Halt

Let's examine what should have been impossible if this was truly just a cooling failure:

1. OTC Price Movements During Frozen CME Pricing

When CME futures markets are halted, over-the-counter (OTC) silver trading continues using last known futures prices for reference. However, multiple traders reported:

- Spot silver "nuked" $1 in minutes after the halt

- This occurred despite no new CME price discovery

- Gold experienced two separate $40 liquidation wicks that instantly recovered

- Bid-offer spreads in gold widened to 20x normal levels

Question: How does spot silver drop sharply when the futures market that provides price discovery is completely frozen?

Possible explanations:

- Large OTC selling by entities with advance knowledge of extended halt

- Market maker repositioning using the halt as cover to adjust exposure

- Algorithmic trading failures causing cascade selling without futures arbitrage

- Coordinated intervention by bullion banks to suppress breakout

2. The "No Quotes Left" Phenomenon

According to a commodity trader source, the silver futures order book had cleared all offer-side quotes just before the halt. This means:

- Every sell order at available prices had been absorbed by buyers

- The next trade would have required sellers to post significantly higher prices

- This is the setup for a price gap that could devastate short positions

- The halt provided time for market makers to reprice and reposition

3. The Instantaneous Recovery Liquidation Wicks

Gold's two $40 drops that immediately recovered are not characteristic of organic selling:

- Real liquidation events show graduated selling over minutes/hours

- Instantaneous recovery suggests algorithmic or automated intervention

- This pattern indicates extreme plumbing stress rather than fundamental selling

- Professional traders described it as the system "testing for liquidity"

The Infrastructure Failure That Wasn't

Let's apply physical security and operational analysis to the cooling failure claim:

Scenario Analysis:

If this was a legitimate cooling failure:

- Temperature monitors should have provided 2-4 hours advance warning

- Free cooling mode should have been automatically engaged

- Emergency protocols should have gradually powered down systems to prevent damage

- Backup chillers should have automatically activated

- CME should have proactively announced expected downtime

- Recovery should have been complete and coordinated, not gradual

What actually happened:

- Abrupt shutdown with no advance warning

- No proactive communication until after markets halted

- 10+ hour outage despite claimed deployment of temporary cooling

- Gradual, piecemeal restoration suggesting improvised rather than planned recovery

- Continued issues with specific contract types even after main markets reopened

Conclusion: This failure pattern is more consistent with:

- Deliberate system shutdown for emergency maintenance

- Critical infrastructure damage requiring extensive repairs

- Planned intervention disguised as technical failure

- Cascading software/network failure blamed on cooling for optics

The Regulatory and Oversight Failures

Where Were the Regulators?

The Commodity Futures Trading Commission (CFTC) and Securities and Exchange Commission (SEC) have overlapping jurisdiction over CME operations. The fact that:

- No advance approval was required for dependency on single data center

- No backup facility requirements for critical infrastructure

- No public post-mortem required after major outages

- No penalty or investigation announced after this incident

...reveals a massive regulatory gap in critical financial infrastructure oversight.

The Google Cloud Migration: Timing and Questions

On November 24, 2025—just three days before the "cooling failure"—CME announced plans to migrate its Globex infrastructure to a dedicated Google Cloud region in Chicago, with preview phases expected to begin in 2026.

Questions this raises:

- Was the November 28 outage related to preliminary migration work?

- Did the announcement trigger concerns about operational readiness?

- Were infrastructure tests conducted that exposed cooling system vulnerabilities?

- Was this outage a catalyst for accelerating the cloud migration timeline?

The proximity of these events suggests they may be connected, though CME has not acknowledged any relationship.

Third-Party Vendor Accountability

CyrusOne's response has been notably limited:

- Generic statement about "chiller plant failure"

- No detailed root cause analysis provided to public

- No timeline for preventing future incidents

- No customer notification beyond CME's statements

For a company hosting infrastructure processing $26.3 million in daily contract volume, this level of transparency is wholly inadequate. Compare this to:

- AWS post-mortems that provide detailed technical analysis of failures

- Azure outage explanations with timeline and remediation plans

- Cloudflare incident reports with specific code changes and architectural decisions

CyrusOne's opacity suggests either:

- Protecting CME from reputational damage by minimizing technical details

- Liability concerns about admitting infrastructure deficiencies

- NDA restrictions preventing full disclosure

- Actual cause was not what was publicly stated

The Broader Implications: When Financial Infrastructure Becomes Weaponized

Systemic Risk in Concentrated Infrastructure

This incident exposes a fundamental vulnerability in modern financial markets:

The Concentration Problem:

- CME Group handles 90% of global derivatives trading volume

- One data center (CHI1 Aurora) hosts this critical infrastructure

- CyrusOne operates 55+ data centers but CME depends on one

- No apparent hot-standby facility capable of immediate failover

Compare this to our cybersecurity practice:

When I conduct security assessments for hospitals, power plants, and Fortune 100 companies, we mandate geographic distribution of critical systems. A hospital's electronic health records don't reside in one data center. A power plant's SCADA systems have offline backups. Fortune 100 companies maintain multi-region failover for critical applications.

Yet the world's largest derivatives exchange—handling trillions in notional value—depends on cooling pipes in one Illinois suburb?

The "Plumbing" Defense

When confronted about market interventions, exchanges and regulators often cite "market plumbing" issues:

- "Protecting market integrity" by halting trading during extreme volatility

- "Ensuring orderly markets" by restricting certain trades

- "System capacity limitations" as justification for strategic failures

This rhetoric masks a more fundamental truth: Market infrastructure can be weaponized to protect institutional interests when retail or foreign participants threaten established positions.

Examples:

- Robinhood/GameStop: Claimed "clearing house capital requirements" forced buy restrictions, protecting short-sellers

- LME Nickel: Cited "disorderly market conditions" to cancel trades, saving Chinese producer from billions in losses

- CME Silver: Claims "cooling failure" halts trading precisely as silver threatens multi-decade breakout

The Political Economy of Market "Failures"

We must ask uncomfortable questions:

Who benefits from these failures?

- Bullion banks with massive short positions in silver and gold

- Institutional market makers needing time to reposition during thin liquidity

- Central banks seeking to suppress precious metals as inflation hedges

- Derivatives dealers exposed to volatility in thinly-traded holiday markets

Who suffers from these failures?

- Retail traders unable to close profitable positions or manage risk

- International participants in Asian and European sessions

- Momentum traders locked out during critical breakout attempts

- Anyone not part of the institutional inner circle with advance knowledge

Lessons for CISOs and Security Professionals

The Third-Party Risk Management Failure

This incident should be required reading in every third-party risk management training:

What CME Got Wrong:

- Sale-Leaseback Without Control: Sold critical infrastructure while maintaining operational dependency

- Single Point of Failure: No redundant facility capable of immediate failover

- Vendor History Ignored: CyrusOne CHI1 had documented infrastructure issues throughout 2025

- Geographic Concentration: All eggs in one Aurora, Illinois basket

- Insufficient SLAs: No penalty clauses for extended outages apparently included in lease agreement

- Inadequate Testing: No evidence of regular disaster recovery drills testing full failover

What CISOs Should Learn:

✅ Never relinquish infrastructure control for cost savings if that infrastructure is mission-critical

✅ Geographic distribution of critical systems is not optional

✅ Active-active architectures should allow immediate failover

✅ Vendor history matters—prior incidents predict future failures

✅ Financial penalties in SLAs should make failures more expensive than prevention

✅ Regular testing of disaster recovery plans with full stakeholder participation

Questions Every CISO Should Ask Their Team:

- What are our single points of failure in critical systems?

- If our primary data center became unavailable for 10 hours, could we operate?

- Do we own or lease our most critical infrastructure?

- What vendor incidents have occurred in the past 24 months that we should factor into risk assessments?

- When was the last time we actually tested our disaster recovery plan with full failover?

The Physical Security Perspective

Working event security at major venues like ACL Festival, Formula 1, and Moody Center, I've learned that redundancy is everything:

- Multiple power feeds from different substations

- Redundant communications across different carriers

- Backup generator capacity for full operational load, not just life safety

- Regular testing of all backup systems under load

- Documented procedures for every failure scenario

Financial markets deserve at least the same operational rigor we provide for concert venues and sporting events.

The Path Forward: Accountability and Reform

What Needs to Change

1. Regulatory Requirements for Critical Financial Infrastructure

The CFTC and SEC must mandate:

- Geographic redundancy requirements for systemically important exchanges

- Maximum allowable downtime before penalties (e.g., 15 minutes, not 10 hours)

- Public post-mortem reports for any outage exceeding 1 hour

- Pre-approval of infrastructure changes affecting critical systems

- Annual disaster recovery testing with regulator observation

- Financial penalties tied to trading volume lost, not fixed fines

2. Exchange Accountability Standards

CME Group should be required to:

- Publish detailed root cause analysis of November 28 outage

- Demonstrate hot-standby capability through live failover test

- Disclose sale-leaseback arrangements and control limitations to shareholders

- Implement real-time redundancy before next trading day

- Compensate market participants for losses due to infrastructure failures

3. Third-Party Vendor Transparency

CyrusOne and similar providers must:

- Report infrastructure incidents to financial regulators within 1 hour

- Provide detailed technical explanations of outages affecting financial markets

- Submit to independent audits of infrastructure reliability

- Maintain public dashboard showing facility health metrics

- Disclose maintenance affecting critical customers 72 hours in advance

The Silver Market Implications

For precious metals investors, this incident confirms what many have suspected:

The paper market can be manipulated through strategic infrastructure "failures" when physical demand threatens to overwhelm the derivatives market.

However, this intervention is a sign of desperation, not strength. The fact that exchanges must resort to halting trading entirely suggests:

- Short positions are more vulnerable than previously understood

- Physical demand is creating pricing pressure that paper markets cannot suppress indefinitely

- The disconnect between paper and physical pricing is reaching breaking point

- Future interventions will be increasingly obvious and desperate

Investment Implications:

- Physical holdings remain outside the paper market manipulation infrastructure

- Extended outages may become more frequent as pressure builds

- Regulatory scrutiny of precious metals markets may finally arrive

- Alternative trading venues may gain importance as CME reliability questioned

Conclusion: The Cooling System That Worked Too Well

The November 28, 2025 CME "cooling failure" will be remembered as either:

Option A: An unfortunate technical failure that coincidentally occurred during a historic precious metals rally, at the exact moment silver was breaking out, on a day when banks borrowed $24.4 billion from the Fed, affecting options expiry worth $600 billion, despite redundant cooling systems and free-cooling weather conditions, at a facility with a history of infrastructure problems, requiring 10+ hours to resolve despite deployment of temporary cooling equipment, with gradual piecemeal restoration suggesting improvised rather than planned recovery.

Option B: A strategic intervention designed to prevent a catastrophic short squeeze in precious metals markets by providing time for market makers to reposition, institutional players to secure funding through Fed repos, and derivatives dealers to manage exposure during holiday-thinned liquidity.

As a cybersecurity professional who has spent 15+ years assessing security infrastructure and responding to incidents, I know which explanation the preponderance of evidence supports.

The markets need cooling all right—cooling of the overheated leverage in the derivatives market, cooling of the regulatory capture that allows exchanges to operate without adequate redundancy, and cooling of the insider manipulation that treats retail and international traders as prey rather than participants.

Until meaningful reform arrives, expect more "cooling failures" whenever the market threatens to move in directions that challenge institutional interests.

The thermodynamic ceiling for financial markets, it turns out, is not in the data center cooling system—it's in the boardrooms where strategic intervention is planned.

Related Resources

From our cybersecurity practice:

- When the Cloud Falls: Third-Party Dependencies and Critical Infrastructure: October 20, 2025 AWS US-EAST-1 outage exposing fatal flaws in modern enterprise architecture

- Microsoft's Azure Front Door Outage: How a Configuration Error Cascaded into Global Service Disruption: October 29, 2025 Azure outage affecting Microsoft 365, Xbox Live, and thousands of customer services

- When Cloudflare Sneezes, Half the Internet Catches a Cold: November 2025 Cloudflare outage analysis and third-party risk management failures

Physical security practice:

- SSAe Physical Security Services: Professional event security and facility protection services

vCISO and Compliance Services:

- CISO Marketplace: Virtual CISO services, incident response, and security assessments

- Compliance Hub: Framework implementation and regulatory guidance

- Breached Company: Cybersecurity breach analysis and threat intelligence